UK customs penalties — scale of HMRC sanctions and how to avoid them

What customs penalties can HMRC impose for errors in UK declarations? Learn the penalty scale, how voluntary disclosure works, and why using a customs broker protects your business.

Author

easyclearance.pl teamPublished

2026-04-20

Updated

2026-06-11

An error in a customs declaration is not merely a formality to correct. In the UK the customs penalty system operates on multiple levels and can affect both small importers and large companies — from fines of a few hundred pounds through to criminal proceedings and seizure of goods. Understanding how HMRC enforces customs law is the first step towards protecting your business.

Legal basis — what underpins the UK customs penalty system?

The UK customs penalty system is primarily governed by:

- Finance Act 2003 (Part 6) — civil penalties for underpayment of duty and VAT,

- Customs & Excise Management Act 1979 (CEMA) — penalties for smuggling and deliberate duty evasion,

- Finance Act 1994 — procedural penalties,

- Taxation (Cross-border Trade) Act 2018 — post-Brexit provisions relating to the UK Global Tariff.

HMRC has broad powers to impose civil penalties by administrative decision (penalty assessment) without the need to refer the matter to court. Criminal proceedings are reserved for the most serious cases.

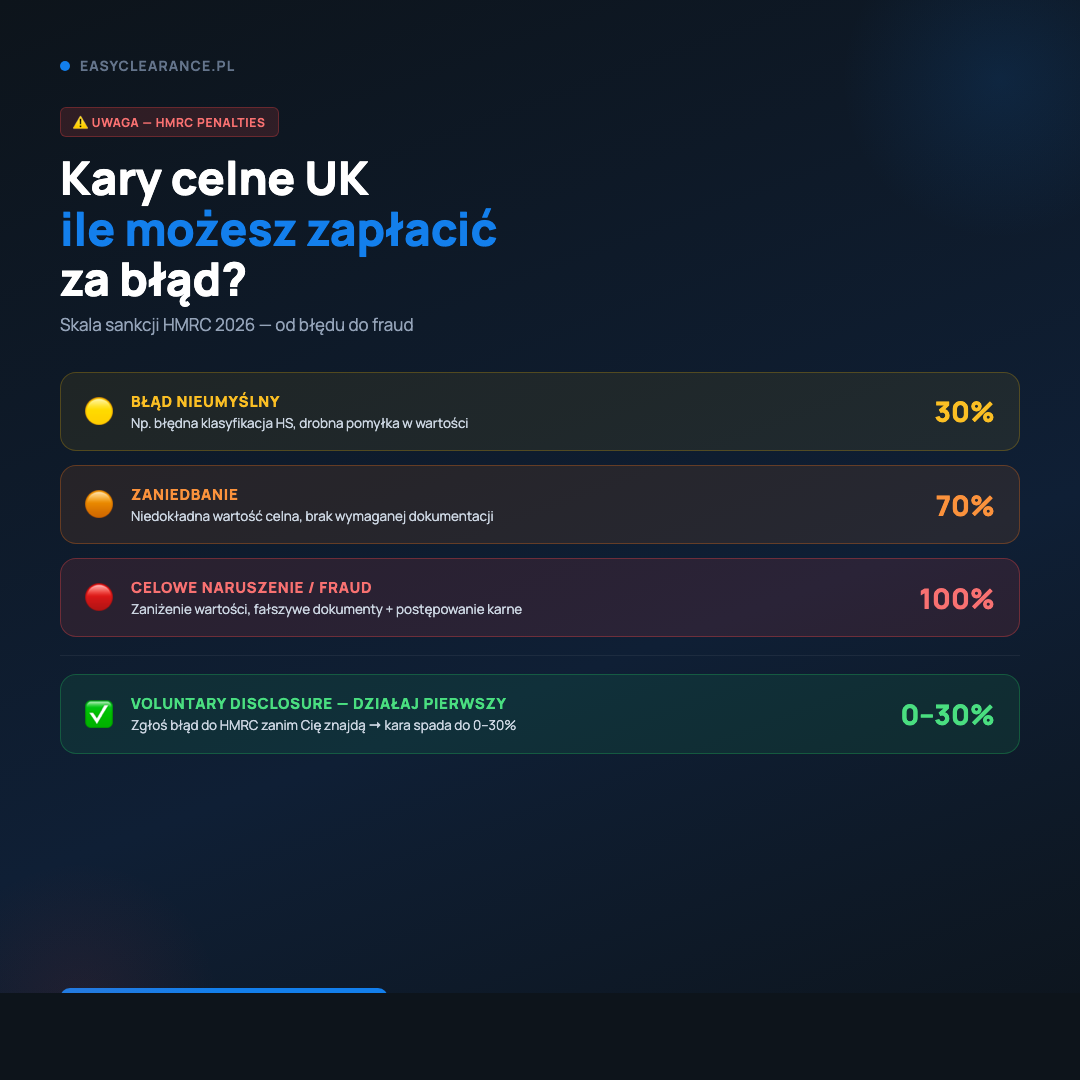

Types of customs penalties and their scale

Civil penalties — administrative sanctions

These are the most common type of penalty, imposed by HMRC through an administrative penalty assessment. The amount depends on the degree of culpability:

| Type of breach | Maximum penalty | How to avoid it |

|---|---|---|

| Error despite reasonable care | 30% of underpaid duty/VAT | Good documentation, HS code verification |

| Failure to take reasonable care | 30% of underpaid duty/VAT | Use a customs broker |

| Carelessness | 30% of underpaid duty/VAT | Regular compliance audits |

| Deliberate action | 70% of underpaid duty/VAT | — |

| Deliberate action with concealment | 100% of underpaid duty/VAT | — |

Important: the penalty is calculated on the amount of underpaid duty and import VAT, not on the value of the goods. If the underpayment is £10,000, a carelessness penalty can add up to £3,000 in additional sanctions.

Procedural penalties

These are imposed independently of the size of any underpayment for:

- failure to submit a declaration on time,

- absence of required documentation during an inspection,

- failure to respond to an HMRC request for documents,

- registration breaches (missing EORI, incorrect details).

Amounts range from £250 to £3,000 per breach and can accumulate.

Criminal penalties — criminal liability

Criminal proceedings are initiated in serious cases of deliberate duty evasion (civil evasion) or smuggling. Legal basis: CEMA 1979 Section 170.

Consequences may include: - up to 7 years' imprisonment for smuggling or falsifying customs documents, - seizure of goods — goods may be taken immediately, without a court order, - forfeiture of the vehicle transporting smuggled goods, - unlimited financial penalties at Crown Court level.

Worth noting: HMRC can impose criminal penalties on both the importer and the customs agent if the agent was aware of or participated in the breach.

Seizure — goods detained by HMRC

Seizure of goods takes place when HMRC has grounds to believe that the goods:

- are being smuggled,

- are connected to a criminal offence,

- do not meet phytosanitary or product safety requirements.

Seizure is immediate — the importer has no right of objection at the moment of seizure itself. A Notice of Claim (appeal) can be submitted within 1 month of the date of seizure to seek return of the goods or compensation.

If the goods are perishable, every hour counts. A professional customs agency can expedite the release procedure.

What does HMRC examine during a post-clearance audit?

A post-clearance audit (PCA) can take place even several years after the clearance. HMRC is entitled to review customs declarations from the last 3 years (for carelessness) or 6 years (for deliberate action).

Areas examined include:

- Tariff classification (HS codes) — was the goods classified under the correct code and was the correct duty rate applied?

- Customs value — does the declared price reflect the actual transaction value? HMRC has access to market price databases and can challenge values that appear below market rate.

- Rules of origin — was a preferential rate applied (e.g. 0% under the TCA) and did the goods genuinely meet the rules of origin?

- Special procedures — were reliefs (ToR, RGR, IPR) applied correctly and were all conditions satisfied?

- Documentation — completeness and consistency: commercial invoice, packing list, CMR, certificate of origin, licences.

No documentation = no evidence = HMRC presumes non-compliance.

How to calculate underpayment — a practical example

A company imports machinery from the UK to Poland via a third party. It classifies the goods under an HS code attracting 0% duty, but the correct code carries 3.7%. Customs value: £80,000.

- Duty underpayment: £80,000 × 3.7% = £2,960

- Carelessness penalty (30%): £888

- Late payment interest (from date of import): ~£150

- Total payable: approx. £4,000 — plus legal handling costs.

Had a customs broker verified the classification before clearance — cost: nil.

Voluntary disclosure — how to reduce a penalty

Voluntary disclosure is a mechanism that allows an importer to self-report an error or underpayment to HMRC before HMRC detects it themselves. The consequences of voluntary disclosure are significantly more lenient than penalties for a detected breach:

- The penalty can be reduced to zero for unintentional errors with full co-operation,

- For deliberate underpayment — reduction to 35% (versus 70% without disclosure),

- No criminal prosecution in the vast majority of cases.

How to make a voluntary disclosure: 1. Prepare a report of errors — which declarations, which lines, what underpayment amount. 2. Submit the application to HMRC via the CDS system or by post to the relevant office. 3. Pay the outstanding debt by the agreed deadline. 4. HMRC issues a decision setting out the final penalty amount.

A customs broker prepares such documents and communicates with HMRC on your behalf.

Compound settlement — reaching agreement instead of going to court

For more serious breaches that might otherwise proceed to criminal court, HMRC often proposes a compound settlement — a financial agreement that concludes the matter without court proceedings. Terms typically involve:

- The importer pays a sum agreed with HMRC (usually a multiple of the underpaid duty),

- No entry on the criminal register,

- The case is closed.

This is a favourable option for both parties — HMRC recovers what is owed without a costly trial, and the importer avoids a conviction.

The role of a customs broker in minimising penalty risk

A good customs broker protects you from penalties on several levels:

- Prevention — correct classification, customs value verification, and rules of origin checks before clearance.

- Documentation — complete and consistent documentation eliminates grounds for HMRC challenge.

- Monitoring — the broker tracks changes to the tariff (e.g. new HS codes, anti-dumping duty rate changes) and keeps clients informed.

- Intervention — during an HMRC inspection the broker represents the client, answers queries, and supplies documents.

- Post-clearance — if an error is discovered, the broker prepares a voluntary disclosure and negotiates terms with HMRC.

[LINK: find out how Easy Clearance protects your clearances] [LINK: see our customs compliance services]

FAQ

What is the maximum customs penalty in the UK for an error in a declaration? For deliberate concealment of an underpayment — up to 100% of the underpaid duty and VAT. For carelessness — up to 30%. Where there was no culpability and the error is corrected promptly — the penalty can be reduced to zero via voluntary disclosure.

Can HMRC review my customs declarations from previous years? Yes. HMRC has the right to carry out a post-clearance audit covering the last 3 years (carelessness) or 6 years (deliberate action). It is advisable to retain all import documentation for a minimum of 6 years.

What is voluntary disclosure and when should I use it? Voluntary disclosure is the voluntary reporting of an error to HMRC before HMRC discovers it themselves. It dramatically reduces penalties — for unintentional errors often to zero. The sooner you disclose, the better.

Can I lose my goods because of a clearance error? Yes — HMRC has the power of seizure in cases of suspected smuggling, falsification of documents, or breach of product safety legislation. Seizure is immediate, and an appeal (Notice of Claim) is possible within 1 month.

Is a customs broker liable for errors in my clearance? It depends on the form of representation. Under direct representation — liability rests with the importer. Under indirect representation — the broker is jointly liable. A reputable broker carries professional indemnity insurance that covers such situations.

Don't risk penalties — entrust your clearance to professionals

Easy Clearance handles imports and exports between the UK and Poland, verifies classifications and customs values, and represents you before HMRC when problems arise.

WhatsApp: +44 7404 091503 Tel: +44 7404 091503

Disclaimer: The information on this page is of a general operational and informational nature and does not constitute legal or tax advice. The price ranges stated are indicative — an exact quote will be provided on receipt of your documents.

Got a similar case?

Send us 3 details: goods, route, Incoterm — we will come back with the right clearance route. We respond 24/7.